Technology Runs Triumphant

By Fauzia Timberlake,

professional options trading coach

June 1, 2026

Market Roundup & The Week in Review

The final week of May brought a definitive statement from the equity markets as large-cap benchmarks defied mounting macroeconomic headwinds to etch their names further into the record books. The S&P 500 logged its seventh consecutive daily gain on Friday, confidently closing out its ninth straight winning week—the longest sustained upward streak since 2023. While structural undercurrents presented plenty of data for both bulls and bears to digest, the aggregate tape remained completely unbothered, firmly propelled by an unquenchable institutional appetite for core technology infrastructure.

The dominant story of the holiday-shortened week was a spectacular verification of the artificial intelligence build-out phase. Enterprise hardware giant Dell Technologies acted as the primary lightning rod, skyrocketing nearly 38% for the week on the back of an 88% year-over-year quarterly revenue explosion fueled by an unprecedented $24.4 billion in standing AI server orders. This massive operational beat sent shockwaves through the entire semiconductor, networking, and data-storage footprint. Institutional desks responded with an aggressive, top-heavy rotation—vividly evidenced by the tech sector gaining over 15% across the month of May alone, even as a quiet majority of the individual S&P 500 industry sectors actually lost ground over the same monthly stretch.

Underneath the headline tech euphoria, the macroeconomic environment grew increasingly complex. The Bureau of Economic Analysis released its April Personal Consumption Expenditures (PCE) report, revealing that headline inflation accelerated to 3.8% year-over-year, while the core reading ticked upward to 3.3%. This persistent price stickiness prompted stern remarks from Federal Reserve leadership, who noted that near-term rate cuts are practically impossible under prevailing conditions, hinting instead that tackling this stubborn inflation could eventually require hiking borrowing costs.

Despite the hawkish central bank commentary, catastrophic pressure on equities was averted due to an aggressive relief wave in the commodity and debt complexes. Momentum built rapidly around reports that the U.S. and Iran have neared a breakthrough 60-day ceasefire memorandum to defuse the regional conflict. The prospect of an imminent peace deal and the subsequent toll-free reopening of the strategic Strait of Hormuz triggered a sharp 10% plunge in global crude oil prices, dragging West Texas Intermediate under $88 a barrel. This steep energy unwind dragged Treasury yields down in sympathy, with the benchmark 10-year yield sliding 12 basis points to finish at 4.45%, offering large-cap growth operators an ideal fundamental runway to charge into June.

Despite lingering geopolitical headline risks and a hawkish tone from the latest Fed minutes, markets repeatedly shrugged off early-week semiconductor capacity worries to push all three major indices to fresh all-time highs by Friday.

Large-cap growth completely dominated the week's tape. QQQ and SPY outpaced small-caps and blue-chips by a wide margin, heavily driven by Friday's explosive post-earnings moves in AI server and hardware providers.

As equities marched to all-time structural highs, the VIX collapsed 5.86% to close at a multi-month low of 15.74.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

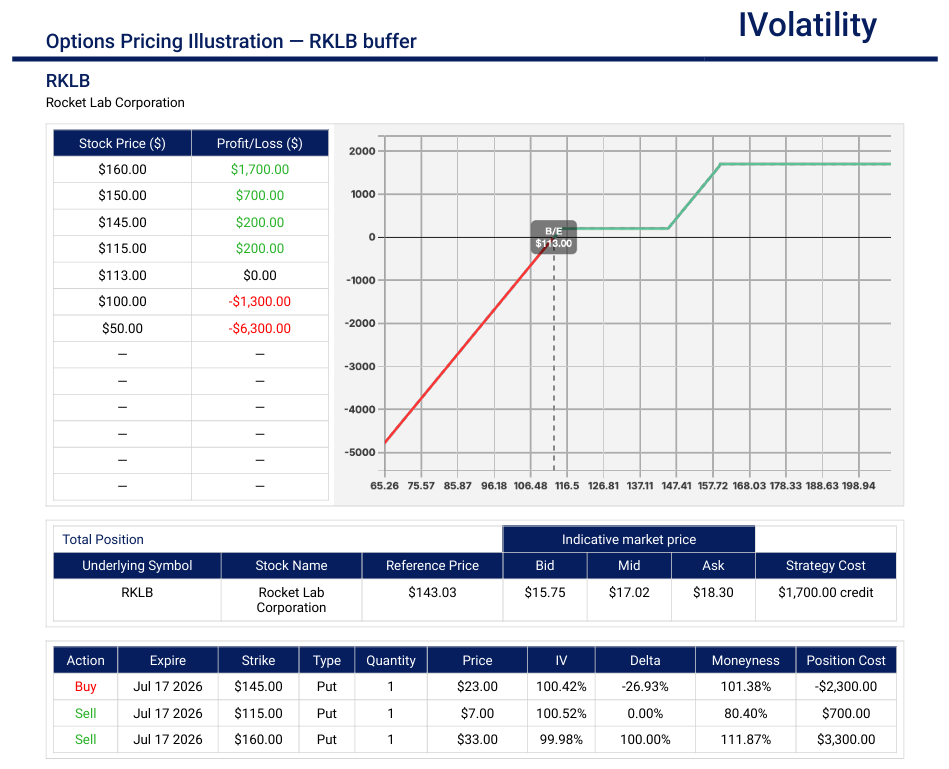

RKLB (closed at 143.54 on Friday, May 29th)

Outlook: bullish

As tech growth runs triumphant across the major indices, capital appears to be quietly rotating into infrastructure plays that provide concrete, long-term operational barriers to entry (moats). Within the aerospace and satellite deployment sector, Rocket Lab (RKLB) has firmly established itself as the premier public vehicle to capture the structural build-out of the low Earth orbit (LEO) megaconstellation economy.

Strategy: Buffer

In the July monthly expiration, buy an ATM put spread and sell an ITM put, deep enough to cover the cost of the put spread. The example strikes used are 115, 145 and 160

Premium collected about $1700 (enough to take breakeven to below 115)

Net Position Delta around +30

Downside breakeven around 112

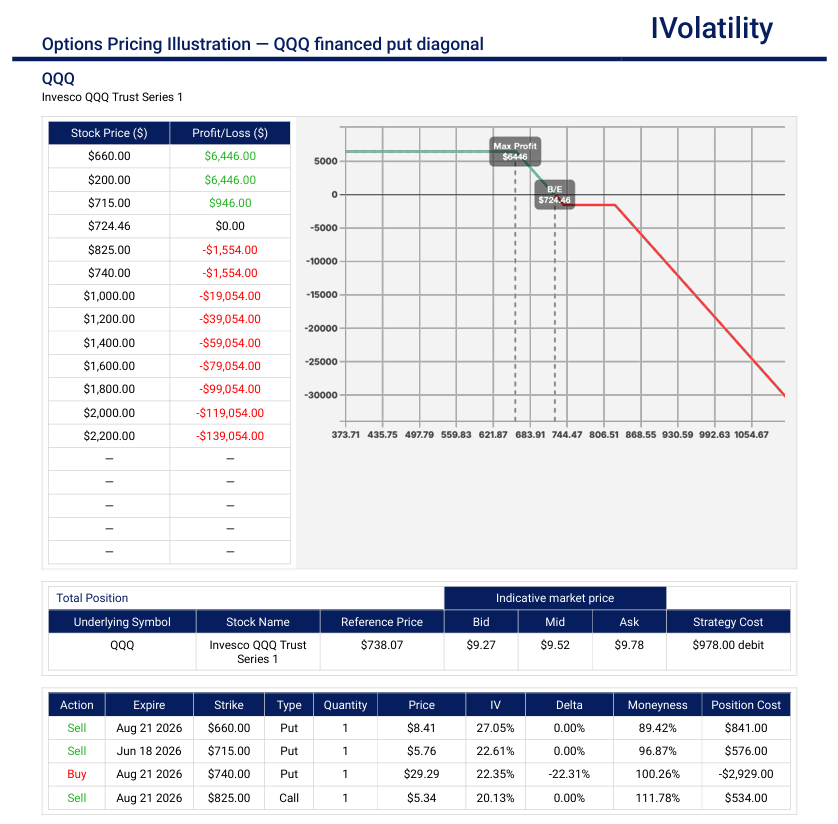

QQQ (closed at 738.29 on Friday, May 29th)

Outlook: neutral, leaning bearish

Building a short-to-medium-term bearish case for the Nasdaq-100 (QQQ) over the next 45 to 60 days means looking beyond daily momentum and focusing on a confluence of structural, seasonal, and macroeconomic factors. With QQQ wrapping up May at an all-time high of $738.31, a tactical downside or consolidation position heading into the summer months can be appropriate.

Strategy: Financed Put Diagonal

For the put diagonal, Buy the Aug21 740put / Sell the Jun18 715put

Partially finance the purchase of the put diagonal by Selling the Aug21 660/825 strangle

Net position delta about -21

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

| SPY | 0.98% | |

| QQQ | 2.13% | |

| IWM | 0.12% | |

| DIA | 0.52% | |

| GLD | 0.35% | |

| BTC/USD | 1.22% | |

| 10-year yield | -1.98% | |

| Crude Oil | -4.27% | |

| VIX | -4.49% |

The driving force behind the equity push was a highly supportive dual-narrative. First, Friday's cool core PCE inflation print dropped 10-year Treasury yields by 11 basis points down to 4.45%, lowering the cost of capital for high-growth names. Second, a steep collapse in global energy inputs offered immediate structural relief to corporate profit margins across the board.

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | 4.50% | |

| FINANCIALS (XL) | -.70% | |

| INDUSTRIALS (XLI) | 0.80% | |

| ENERGY XLE | -5.31% | |

| HEALTHCARE (XLV) | -0.20% | |

| UTILITIES (XLU) | -2.00% | |

| MATERIALS (XLB) | 1.74% | |

| REAL ESTATE (XLRE) | -1.20% | |

| CONSUMER STAPLES (XLP) | -3.09% | |

| CONSUMER DISCRETIONARY (XLY) | 1.50% |

Sector performance split aggressively this week along cyclical and growth boundaries. High-margin technology completely detached from the rest of the tape, while defensive value groups experienced deep institutional distribution. The primary catalyst was a major shift in enterprise capital expenditures, as corporate earnings underscored that technology infrastructure spending is cannibalizing traditional defensive budgets.

Underneath the headline tech run, a massive structural unwind in the energy complex redefined late-week margin expectations. As energy input costs collapsed, capital actively rotated into materials and select industrial cyclicals, helping to establish a firm fundamental floor across supply-chain heavy sectors while severely punishing pure-play energy producers.

Notable gainers for the week of May 25th – May 29th

The shortened trading week belonged entirely to big-ticket technology components and high-margin software vendors. Record-breaking enterprise capital expenditures and explosive guidance updates acted as the primary engines for individual equity momentum.

The sheer velocity of Dell's run showed that institutional portfolios seem to be completely unwilling to miss the physical build-out phase of computing infrastructure. The spillover effect into secondary data providers like NetApp indicates broad-based, structural sector depth rather than isolated momentum.

DELL (+37.96%): Delivered a massive Q1 earnings beat and aggressively lifted its full-year forward revenue guidance, driven by a record wave of institutional orders and insatiable enterprise demand for its AI-optimized hardware computing servers.

NTAP (+22.39%): Caught an immense sympathy wave across the data-center infrastructure space after posting a substantial top-and-bottom-line earnings beat paired with highly optimistic forward projections for enterprise cloud storage management.

NOW (+14.40%): Accelerated higher on heavy institutional volume following a series of high-profile cloud software automation contract expansions, highlighting deep corporate pricing power and high seat-retention metrics.

IBM (+12.71%): Led the blue-chip growth rally after receiving a major institutional broker upgrade that highlighted exponential pipeline growth and rapid monetization within its generative AI consulting division.

CRM (+8.46%): Staged a strong tactical rebound off intermediate technical support levels as enterprise cloud spending stabilized and fears of cooling software seat licensing subscriptions subsided.

Notable losers for the week of May 25th – May 29th

The overriding theme driving the week's notable decliners was strict institutional punishment for asymmetric earnings results. Wall Street showed absolutely zero tolerance for companies that managed top-line or bottom-line beats but paired them with structural margin contraction or defensive forward projections. This was most visible in the enterprise security and hardware space, where high-multiple growth names like Zscaler were heavily liquidated after cutting free cash flow outlooks to fund higher capital expenditures.

Outside of technology, individual equity drawdowns across the retail and medical device footprints reflected a mix of cautious domestic consumer behavior and back-end inventory friction. Disappointing quarterly foot traffic metrics, unfavorable LIFO inventory accounting adjustments, and cautious multi-quarter guidance updates prompted automated portfolio distributions. As institutional desks aggressively harvested capital out of underperforming value and cyclical positions to chase the historic large-cap hardware breakout, these fundamentally vulnerable names quickly bore the brunt of the week's sharpest sell-offs.

ZS (-23.35%): Sold off violently to become the week's worst-performing stock as a combination of cooling cybersecurity billings projections and downward revisions to corporate cloud defense spending rattled growth investors.

BSX (-16.36%): Faced intense, high-volume institutional distribution after an unexpectedly cautious intermediate-term forward guidance update concerning medical device margin pressures over the upcoming fiscal quarters.

GAP (-15.40%): Dropped sharply post-earnings after receiving high-profile analyst downgrades from both JPMorgan and Evercore ISI, citing fading retail execution and near-term inventory management overhead.

AZO (-13.84% DOWN): Experienced steep weekly selling pressure as softer domestic consumer automotive retail foot traffic and an unexpected dip in quarterly profit margins triggered broad risk-off selling.

S (-11.60% DOWN): Slipped backward despite a mid-week broker upgrade to "Buy" at BofA, as institutional portfolios aggressively rotated out of mid-cap enterprise software lines to free up capital for mega-cap AI server hardware plays.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

US markets were closed in observance of Memorial Day.

While domestic equity trading was dark in observance of the Memorial Day holiday, global markets reacted sharply to a major shifting macro narrative: a potential diplomatic breakthrough in the Middle East.

Tuesday's Markets and News:

Primary capital markets reopened to a massive surge in corporate credit issuance, as issuers raced to lock in borrowing costs following Monday's drop in global yields. Equity underwriting also saw sharp execution, with several major follow-on offerings pricing smoothly.

Technology absolutely dominated the session, carrying both the S&P 500 and the Nasdaq to fresh record-shattering closes. In sharp contrast, classic cyclicals dragged the Dow Jones Industrial Average down 0.2% to 50,461.68, exposing a clear momentum split. The semiconductor sector experienced a historic stampede, specifically led by an explosive run in Micron Technology (MU). Following public praise regarding the company's aggressive state-side manufacturing infrastructure investments, the Idaho-based memory provider cleared a monumental $1 trillion market valuation for the first time in history, dragging the entire tech ecosystem up with it.

Domestic crude markers finished highly fragmented as the market struggled to match early-session optimization with fresh geopolitical headlines. While international Brent contracts tick slightly higher due to underlying regional friction, domestic West Texas Intermediate (WTI) slipped further down toward $90 a barrel.

A major slowdown in Chinese crude imports heavily eased near-term supply strains on Asian markets. This drop in structural demand perfectly offset fears of an immediate regional escalation, prompting light sweet crude to trade heavy all afternoon.

Treasury yields found a firm floor after Monday's global drop, trending marginally higher across the short end of the curve during standard domestic hours. Despite soft housing data, bond traders kept their focus locked on the upcoming core Personal Consumption Expenditures (PCE) print scheduled for Friday. This limited any deeper, unhedged accumulation of paper.

Gold gave back a portion of its early holiday advances, consolidating its position just below the $4,560 per troy ounce mark. The persistent tech-led sprint in U.S. equities pulled speculative interest directly away from alternative safe havens, drawing capital out of raw gold holdings and back into high-beta tech underlyings.

- S&P 500: 7,519.12 (+0.6%)

- Nasdaq Composite: 26,656.18 (+1.2%)

Wednesday's Markets and News:

Capital market primary operations saw immense, highly active order-book depth. Secondary credit markets enjoyed massive volume as investment-grade corporate issuance successfully absorbed heavy mid-week allocations.

Technology was a tale of narrow but explosive leadership that safely held the major growth indices in green territory. While cyclicals and select industrials experienced a fragmented session, retail saw pockets of extreme buying strength.

The semiconductor space caught a powerful tailwind following massive retail earnings beats from consumer names like Abercrombie & Fitch and Bath & Body Works, demonstrating pockets of immense pricing power. This retail-led reassurance allowed tech-focused growth investors to confidently add risk back into highly concentrated, AI-infrastructure mega-caps.

Energy underlyings faced persistent selling pressure, completely underperforming the broader market. Domestic West Texas Intermediate (WTI) fell more than 4% to settle around $93.00 a barrel, while Brent crude dropped below the $99.00 level.

The main driver was a surprise inventory build coupled with broader technical selling as crude fell back down to mid-April price support levels. This steep energy pullback put an immediate damper on oil-and-gas equities, capping the day's structural gains for the broader S&P 500 index.

Fixed-income assets experienced a steady relief bid, pulling sovereign interest rates down across both the short and long ends of the domestic curve. Softening global energy costs significantly cooled near-term headline inflation projections. This structural relief allowed Treasury yields to ease considerably, completely lifting pressure off equity valuations and giving institutional desks a greener light to maintain deep risk exposure.

Precious metals traded strictly in a tight, defensive sideways pattern, underperforming the broader equity landscape to close marginally lower on the day. With the major equity indices persistently grinding out fresh daily nominal records and Treasury yields stabilizing, speculative capital smoothly rotated directly away from alternative safe havens and backed back into high-margin corporate debt and primary market risk.

- S&P 500: 7,520.36 (+0.02% / +1.24 pts)

- Nasdaq Composite: 26,674.73 (+0.07% / +18.55 pts)

Thursday's Markets and News:

Capital markets weathered a massive, multi-layered data dump on Thursday, shrugging off an early-morning dip to push the major benchmarks to a trifecta of new all-time record closes. Pre-market futures faced pressure after conflicting economic indicators. The second reading of Q1 2026 GDP showed economic growth decelerating, driven by a cooling consumer. Conversely, April Durable Goods Orders shattered expectations by exploding +7.9% month-over-month, showcasing that core enterprise business spending remains incredibly resilient.

The critical catalyst that turned the afternoon green was a sharp unwind of geopolitical risk premiums. High-profile reports crossed the wires indicating that a 60-day Middle East ceasefire memorandum was rapidly gaining traction. West Texas Intermediate (WTI) crude plummeted down toward $91 per barrel, dragging the Energy sector (XLE) lower but offering immediate inflationary relief to the bond market. The 10-year Treasury yield eased to 4.47%, clearing a major hurdle for growth stocks.

The corporate tape provided plenty of fundamental fuel for the afternoon index-level push. Dollar Tree (DLTR) skyrocketed +18.0% after printing a robust 7.2% jump in quarterly net sales and a massive 19.7% spike in EPS, proving discount retail execution remains potent. Names like Snowflake (SNOW) and Datadog (DDOG) caught aggressive institutional inflows. Sentiment was further amplified by Goldman Sachs raising its year-end S&P 500 target to 8,000, citing massive, unyielding AI infrastructure capex.

Energy underlyings caught a noticeable stabilizing bid, clawing back a portion of the deep losses sustained during the first half of the week. Benchmark domestic West Texas Intermediate (WTI) recovered to settle near $91.00 a barrel, while global Brent crude climbed back toward $96.00.

Government fixed-income products caught a highly visible, late-session wave of accumulation, effectively dragging yields lower across both the 2-year and 10-year notes. The 10-year Treasury yield drifted down to settle near 4.47%, while the short-term 2-year yield fell back toward 4.03%.

Gold underlyings traded with moderate, choppy volatility, managing a modest green close on the day but continuing to face heavy structural overhead. On one hand, a cooling of near-term Treasury yields and a softening dollar usually push the precious metal higher. However, because equity indices were simultaneously setting nominal records, spec capital stayed highly focused on risk-on tech asset classes, strictly capping gold's safe-haven upside.

- S&P 500: 7,563.63 (+0.6% / +43.27 pts)

- Nasdaq Composite: 26,917.47 (+0.9% / +242.74 pts)

Friday's Markets and News:

The Capital Markets capped an incredibly busy week for underwriting syndicates and corporate treasuries. High-grade and high-yield issuance lines closed early ahead of the weekend, but block-trading desks handled considerable institutional volume as portfolio managers rebalanced books into the month-end close.

The favorable core PCE data from the morning session triggered an immediate collapse in the CBOE Volatility Index (VIX), which dropped down to a 4-month low of 15.74. With volatility heavily suppressed, institutional derivative desks aggressively priced and executed complex structured equity products, while primary liquidity channels easily absorbed large-scale capital deployments without denting the broader indices' record-shattering run.

Big tech and AI-adjacent hardware providers staged another spectacular showing, pushing the Nasdaq to yet another record close. Industrials also saw robust pockets of accumulation, while the Dow Jones Industrial Average surged 0.7% to confidently clear the historic 51,000 milestone.

The session was completely electrified by Dell Technologies (DELL), which skyrocketed 33.1% to a lifetime high of $420.91. Dell's massive Q1 earnings beat and subsequent historic guidance increase—fueled by insatiable enterprise AI server demand—sparked an industry-wide chain reaction, lifting hardware peers like Super Micro Computer (+8.3%) and NetApp (+17.2%) alongside them. Robinhood.

Government fixed-income notes put together a major late-week rally, pushing bond prices higher and dropping yields down to multi-week lows across the entire curve. The short-term 2-year note plummeted to 3.98%, while the benchmark 10-year Treasury yield slid down to 4.45%.

The macro spotlight belonged entirely to April's core Personal Consumption Expenditures (PCE) Prices index—the Federal Reserve's preferred inflation gauge. Core prices rose just 0.2% month-over-month, undercutting the 0.3% Wall Street estimate. This cooling of underlying inflationary pressures, paired with an unexpected 13.5-point spike in the Chicago PMI to 62.7, signaled a healthy economic expansion without the threat of overheating

Energy markets remained highly defensive, extending their weekly declines to wrap up a deeply challenged month. Benchmark domestic West Texas Intermediate (WTI) fell further, settling at $87.93 per barrel, while global Brent crude drifted near $92.50.

Persistent concerns regarding slowing crude imports from major Asian economies, paired with rising domestic inventory builds earlier in the week, kept a heavy lid on physical oil. This downward trend prompted institutional systematic funds to trim energy equity allocations further, dragging down sector underlyings.

Gold underlyings caught a solid intraday bid, reversing Thursday's choppy trend to finish the week in green territory. The precious metal directly capitalized on the morning's soft core PCE print. The subsequent tumble in Treasury yields and an unwinding of defensive dollar positions provided an immediate structural lift to non-yielding assets, drawing fresh technical buyers back into gold contracts.

- S&P 500: S&P 500: 7,580.06 (+0.22% / +16.43 pts)

- Nasdaq Composite: 26,972.62 (+0.20% / +55.15 pts)

Notable Earnings (June 1st – 5th)

While the broader Q1 earnings season is winding down, this week features high-impact reports from major players in cybersecurity, enterprise software, retail, and tech-adjacent hardware. Here is what to expect and what will drive the market reaction:

- Analysts expect massive earnings growth from Broadcom (+51% year-over-year to $2.39 EPS) and strong Annual Recurring Revenue (ARR) guidance from CrowdStrike targeting the $6.5 billion mark for the fiscal year.

- The market will look past simple top-line beats to focus on forward guidance and how successfully these platforms are selling high-margin, AI-native platforms (like CrowdStrike's Falcon Flex). Look for signs of "buyer fatigue" or spending delays in corporate IT budgets, which could drag down the tech sector if guidance comes in soft.

- Dollar General is riding a wave of low expectations but a recent sector lift from competitor Dollar Tree, while Lululemon is expected to show softer North American revenue ($2.4B–$2.43B range) following a tough, promotional environment.

These three names perfectly capture the structural split in consumer health. For Dollar General, the focus is on whether lower-income consumers are continuing to trade down into essentials. For Ulta and Lululemon, the market will scrutinize full-price selling vs. markdowns and gross margins to see if mid-to-high income discretionary spending is showing deeper cracks.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, June 1st: HPE

Tuesday, June 2nd: PANW

Wednesday, June 3rd: MDT / AVGO / CRWD

Thursday, June 4th: DOCU / LULU

Friday, June 5th: no notable earnings reports on deck

Economic Calendar (June 1st – 5th)

The clear focal point for the market this week will be Friday's May Jobs Report (Non-Farm Payrolls), alongside key manufacturing and services data earlier in the week to gauge economic momentum.

Friday's jobs data is the main event. Consensus points to a modest cooling down with 102,000 jobs expected (down from April's +115,000) and the unemployment rate ticking up slightly to 4.4%.

- The Bull Case: A reading hovering right around consensus pairs with a manageable 0.2% wage growth, supporting hopes for economic normalization without triggering immediate recession fears.

- The Bear Case: A blowout number (above 150K) will reignite fears of structural inflation, while a sharp disappointment (below 70K) will raise alarms that the labor market cooling is happening too quickly.

- Monday, June 1st:

ISM Manufacturing PMI

Construction Spending MoM - Tuesday, June 2nd:

JOLTS Jobs Report - Wednesday, June 3rd:

ADP Employment Change - Thursday, June 4th:

Weekly Initial Jobless Claims - Friday, June 5:

Non-Farm Payrolls

Unemployment Rate

verage Hourly Earnings MoM

Blue Sky Horizons

The Great Migration to the Edge

Building on last week's discussion of The Great Migration to the Edge, the structural shift away from massive centralized cloud data centers toward localized processing is accelerating. While the cloud isn't disappearing, the economic and physical realities of data transmission are redrawing the map of technology infrastructure.

Three core tailwinds are sustaining this momentum:

The Physics of Latency: As real-time Artificial Intelligence inference, autonomous systems, and industrial automation expand, the millisecond delays required to transmit data to a centralized cloud server and back are no longer viable. For applications requiring split-second decisions—such as computerized manufacturing safety, autonomous driving telemetry, or high-frequency automated execution—the time lag imposed by physical distance becomes a critical failure point. Processing data at the edge eliminates this geographical overhead, allowing computation to occur at the exact point of ingestion and enabling true sub-millisecond responsiveness.

The Bandwidth Bottleneck: The sheer volume of telemetry data generated by billions of connected Internet of Things (IoT) devices is rapidly outstripping global network capacity. Trying to stream a continuous, unrefined firehose of raw data from industrial sensors, smart utility grids, and connected vehicle fleets across standard networks to a distant, centralized cloud data center clogs available bandwidth and drives up data transport costs. By shifting processing to the edge, infrastructure architectures can sift, filter, and analyze this information at the point of ingestion—transmitting only critical, high-value summaries back to the cloud and preserving precious network capacity.

The IoT (Internet of Things) refers to the vast network of physical objects—"things"—that are embedded with sensors, software, and processing power, allowing them to connect to the internet and exchange data with other devices and systems.

In the context of the edge computing discussion, these aren't just consumer gadgets like smart thermostats or wearable fitness trackers. They include massive industrial and infrastructure components, such as:

- Industrial Sensors: Equipment on factory floors monitoring vibration, temperature, and machine health.

- Smart Grid Infrastructure: Connected regular and high-voltage meters tracking real-time electricity distribution.

- Connected Vehicles: Fleet trucks and autonomous vehicles continuously transmitting telemetry, traffic, and spatial data.

- Municipal Infrastructure: High-definition traffic cameras, environmental monitors, and automated transit systems.

The "bottleneck" occurs because these billions of devices generate a continuous, massive firehose of raw data. Trying to stream all of that unrefined data across standard networks to a distant cloud data center clogs the bandwidth, which is why processing and filtering that data right at the "edge" (near the device itself) has become so critical.

Data Sovereignty & Privacy: Localized data residency requirements and tightening compliance protocols increasingly mandate that sensitive information remain within strict regional or organizational boundaries. Sending proprietary data, financial records, or personal telemetry to centralized, multi-tenant cloud facilities frequently triggers regulatory friction and heightened security vulnerabilities. Edge architecture elegantly solves this dilemma by keeping data localized on-premise or within designated regional nodes, allowing enterprises to filter and secure information natively before any high-level data summaries are transmitted over external networks.

Thank you for reading. Until next week's close,

Safe Trading!

Fauzia Timberlake

About the Author: Fauzia Timberlake is a professional options coach and financial strategist specializing in risk management and portfolio architecture for self-directed investors. She is Founder and Managing Partner of Option Engines.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the Trade Ideas tab on our website.